All Categories

Featured

Table of Contents

Routinely reconciling bank and credit card declarations makes sure that monetary records accurately reflect actual transactions. This procedure includes comparing accounting records with bank statements to recognize inconsistencies, such as missing out on payments or unapproved charges. Reconciliation helps avoid mistakes, find scams, and ensure that financial reports are based upon accurate data.

Small company owners should track hours worked, account for advantages, and comply with labor laws and tax policies. Proper payroll management not only ensures employees are paid precisely and on time however also helps businesses prevent legal concerns and charges connected to tax withholding errors. Financial reports offer company owner with insights into their company's financial health and performance.

Without routine financial reporting, little services might have a hard time to comprehend their monetary position and make notified strategic choices. The very first step in managing your own bookkeeping is establishing a structured system for tape-recording financial deals. This includes establishing classifications for income and expenses, organizing invoices and invoices, and maintaining precise records of all business transactions.

Small company owners need to choose between money and accrual accounting to track their finances. Cash-basis accounting records income when payments are gotten and expenditures when they are paid, making it basic and suitable for small companies with simple deals. In spite of its simpleness, cash-basis accounting does not offer an accurate monetary image, since it does not account for exceptional invoices or unpaid costs.

The accrual technique, on the other hand, records income when a sale is made (even if payment hasn't been gotten) and expenditures when they are incurred (despite when they are paid), supplying a more precise long-term monetary image. It requires more bookkeeping effort and might lead to money flow problems if not closely kept an eye on.

Reducing Retail Operational Expenses to Improve ROI

Accounting software application, such as Finaloop, automates many accounting tasks, lowers errors, and produces financial reports with ease. Brand name owners ought to weigh factors like company size, deal volume, and the need for automation when deciding between spreadsheets and dedicated accounting software. Cloud-based accounting options allow service owners to automate monetary jobs such as transaction categorization, invoicing, and bank reconciliations.

Cloud accounting likewise provides up-to-date monetary information, making it simpler to track service performance in real-time and cut out the need for accountants. While DIY accounting works well for lots of small company owners, there comes a time when outsourcing may be more beneficial. If accounting jobs end up being too complex, consume excessive time, or cause frequent mistakes, hiring an expert accountant (or using software particularly customized towards your company, like Finaloop) can assist.

Outsourcing bookkeeping enables business owners to focus on core operations while making sure financial records stay precise and compliant. When trying to determine which bookkeeping software is best for little organizations in 2025, it is essential to get out of the box and search for little service accounting software besides quickbooks.

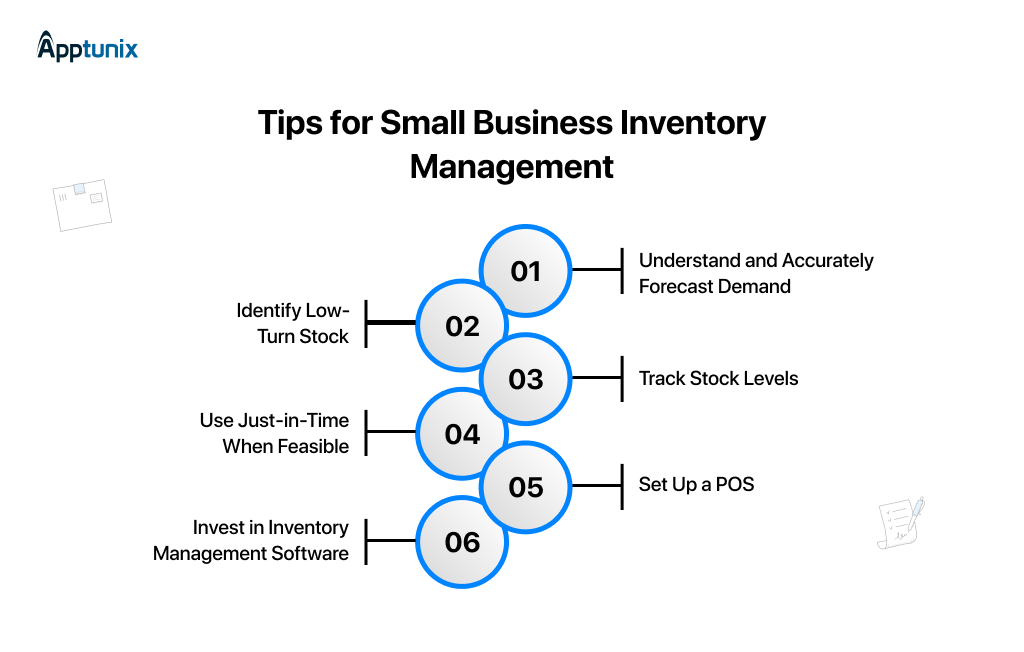

How to Manage Store Inventory Tracking

It uses an ecommerce-dedicated inventory management option developed into accounting software application, a prebuilt ecommerce-focused chart of accounts, accounts receivable and payable management, automated transactions classification, automated reconciliation, and tax ready books. The platform perfectly incorporates with online shop platforms like Shopify or Woocommerce and markets like Amazon and Walmart.

Finaloop integrates with your payment processors, checking account, and online shops for three-way reconciliation orders to payouts to organization savings account and offers accrual versus cash-basis versatility. In addition, it offers a team of internal bookkeepers and 24/7 client assistance. Finaloop's mix of automation and professional accounting services makes it a time-saving and cost-effective option for company owner who want accurate, problem-free financial management.

It provides multi-currency support, stock management, and automated transaction matching, links to all significant accounts, and tracks charges, taxes, and revenue across sales channels to allow historical reports and forecasting. However, QuickBooks is software-only and not a service, suggesting users should have some bookkeeping knowledge to get the most out of it (or employ an accountant).

The platform likewise has a high knowing curve for beginners, and its chart of accounts is not optimized for ecommerce accounting. Xero stands apart with over 800 integrations with third-party applications. The platform offers inventory management, double-entry accounting, bank reconciliation, expenditure tracking with classification guidelines, an invoices and quotes generator, and a customizable control panel.

How to Manage Store Inventory Tracking

It also supplies a hassle-free function for sending quotes, recurring invoices, and pointers. Reports are simple to view and customize, making it an excellent choice for mid to large-size companies. Like QuickBooks, Xero is accounting software application just, requiring DIY accounting by you or an accountant. App combinations cost an extra cost depending on the platform added.

{kind=link}

Latest Posts

Automating Team Rostering to Enhance Productivity

Why Operational Automation Drives Higher Financial ROI

Proven Expense Saving Methods to Boost ROI